Orladeyo: A Tough Pill to Swallow for Competitors in the HAE Space

Key Takeaways

- The hereditary angioedema (HAE) market continues to shift from on-demand treatments to prophylactic treatments, with prophylactic prescriptions growing from ~70% prescription share in 2021 to ~85% in 3Q2023

- Orladeyo prescription share has grown to ~18% and continues to capture a steady rate of patient switches from marketed prophylactic injectables including Takhzyro, Haegarda, and Cinryze

- Although patient persistence trends for Orladeyo are more durable relative to Haegarda and Cinryze, persistence looks to be comparable relative to market leader Takhzyro

In December 2020, BCRX’s Orladeyo made history as the first FDA-approved oral option to prevent hereditary angioedema (HAE) attacks. Despite being later-to-market in a crowded HAE landscape, Orladeyo’s differentiated route of administration has helped BCRX win market share from on-demand therapies and compete with injectable options like Takhzyro (TAK) and Haegarda (CSL).

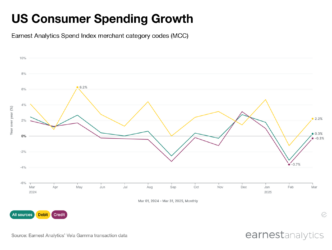

Prophylactic share of the HAE prescriptions has grown by ~20% since Orladeyo’s approval

Contact Sales for more details.

HAE patients can manage acute angioedema attacks with on-demand treatments that provide immediate relief following HAE attacks (e.g., Berinert, Firazyr, Ruconest, Kalbitor), whereas prophylactic options reduce the need for on-demand treatment by decreasing the frequency and severity of attacks. In recent years, the prophylactic market has cannibalized a significant portion of the on-demand market. At a recent conference, BCRX management estimated that the HAE market is roughly 70% prophylactic and 30% on-demand. Earnest data indicates that, as the on-demand market steadily contracts, the prophylactic market has continued to grow and now represents ~85% of HAE prescription volume. BCRX management has noted that patients are sticky to prior injectable therapies, which as Earnest data shows manifested in relatively flat growth following launch. However, in the past two quarters growth has accelerated with BCRX’s Orladeyo accounting for ~18% of total HAE prescription volume in 3Q2023.

Patients that prefer Orladeyo’s oral administration are switching from marketed injectable therapies like Takhzyro, Haegarda, and Cinryze

Contact Sales for more details.

Earnest data captures patients switching from marketed HAE prophylactic therapies (i.e., Takhzyro, Haegarda, and Cinryze) to Orladeyo, which offers the advantage of oral administration. Over Orladeyo’s full history, our data suggests that on average ~47% of patients using Orladeyo (who were previously on a direct competitor) were formerly using Takhzyro, the current market leader. Orladeyo’s growth in the market mirrors Takhzyro and Haegarda’s rise, as patients also preferred subcutaneous administration over Cinryze’s intravenous infusion.

Orladeyo demonstrates similar patient persistence to Takhzyro, but holds a slight advantage over Haegarda and Cinryze

Contact Sales for more details.

Like many other rare diseases, HAE has a relatively limited addressable patient population. In a therapeutic area with low prevalence, patient retention is critical for maintaining and growing market share. Earnest data indicates that patients on Orladeyo are more persistent relative to Cinryze and Haegarda, but overall persistence trends are comparable between Orladeyo and the current market leader Takhzyro. This trend is likely driven by Haegarda and Cinryze’s more onerous dosing schemes – Cinryze is administered via intravenous infusion and Haegarda requires a twice-weekly subcutaneous injection. In contrast, Takhzyro only requires a subcutaneous injection every two weeks and Orladeyo is a once-daily pill, both providing more convenient dosing for patients.

BCRX is projecting $1 billion in Orladeyo sales by the end of the decade. Can Orladeyo maintain its current rate of new-to-brand acquisitions and grow its patient base to meet this sales target? Continue tracking Orladeyo utilization and competitive dynamics within the HAE market with Earnest data.