Holiday Spending Slowed as Inflation Hit Lower Earners

Sign up for free to explore holiday consumer spending data in Earnest Dash.

Powered by Earnest’s Vela spend dataset.

Key takeaways:

- Consumer holiday spending growth decelerated materially from 2021 levels

- YoY consumer spending growth continued to slow on a monthly basis into December

- High income consumers outspent their low income peers during the 2022 holiday shopping season

- Lululemon, Nike, Shein, The RealReal, and Ulta Beauty all shined and grew double digits

Consumer holiday spending measured by the Vela credit and debit card data in Earnest Analytics Spend Index (EASI) increased 5.9% YoY in 2022, a stark contrast from the significant demand growth experienced in the 2021 holiday season but relatively in-line with historical periods as multi-decade high inflation continues to benefit nominal growth. In 2022, holiday spending growth was driven by similar levels of transaction and average ticket growth, though transaction growth was much lower than pre-pandemic levels, a potential sign that inflation continues to squeeze consumer budgets.

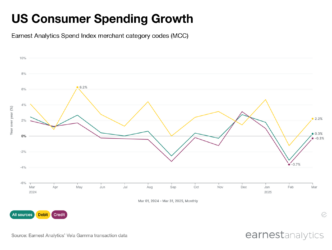

YoY Consumer Spend Growth Continued to Decelerate On A Monthly Basis, Albeit At A Slower Pace

Powered by Earnest’s Vela spend dataset. Access chart in Dash.

Although YoY holiday spending growth accelerated moderately from early holiday season trends, YoY consumer spend growth continued to decelerate on a monthly basis in December 2022 to 5% despite several retailers guiding for demand to strengthen as they approached the holidays. The persistent monthly slowdown through the holiday season could be the result of ever-earlier holiday promotions pulling holiday demand into October.

High Income Consumers Outspent Low Income Peers

Powered by Earnest’s Vela spend dataset. Excludes spending when income is not available. Access chart in Dash.

From the onset of the pandemic through April 2021, low income consumers outperformed their high income counterparts largely due to stimulus payments and enhanced unemployment benefits. However, trends reversed in 2022; a dynamic that continued into the holiday season where high income consumers materially outspent their low income peers. Low income consumers actually slowed their spend from November through December.

Spending Steadily Leaning to First Half

Powered by Earnest’s Vela spend dataset.

Consumers spent 49.0% of their total holiday dollars in the first 31 days of the holiday season in 2022, remaining essentially flat from the prior year. This despite an extra Saturday falling prior to Christmas, Hanukkah falling later on the calendar, and historically earlier shopping in 2021 due to concerns about inventory shortages. This all suggests consumer demand may not have picked up as strongly in the back half of the holiday season as certain retailers anticipated.

Online Penetration Remains Above Pre-COVID Levels

Powered by Earnest’s Vela spend dataset.

The share of consumer dollars spent online was largely consistent with 2021 as 2022 online share remained multiple points above pre-pandemic levels across most major categories; further solidifying the view that certain shopping habits developed during the pandemic may be here to stay. Apparel & Accessories, Electronics, General Merchandise, Grocers, Occasion & Gifts, and Pets all saw increased online penetration by at least 5 points since 2019, while Health & Beauty was the only major category to decline.

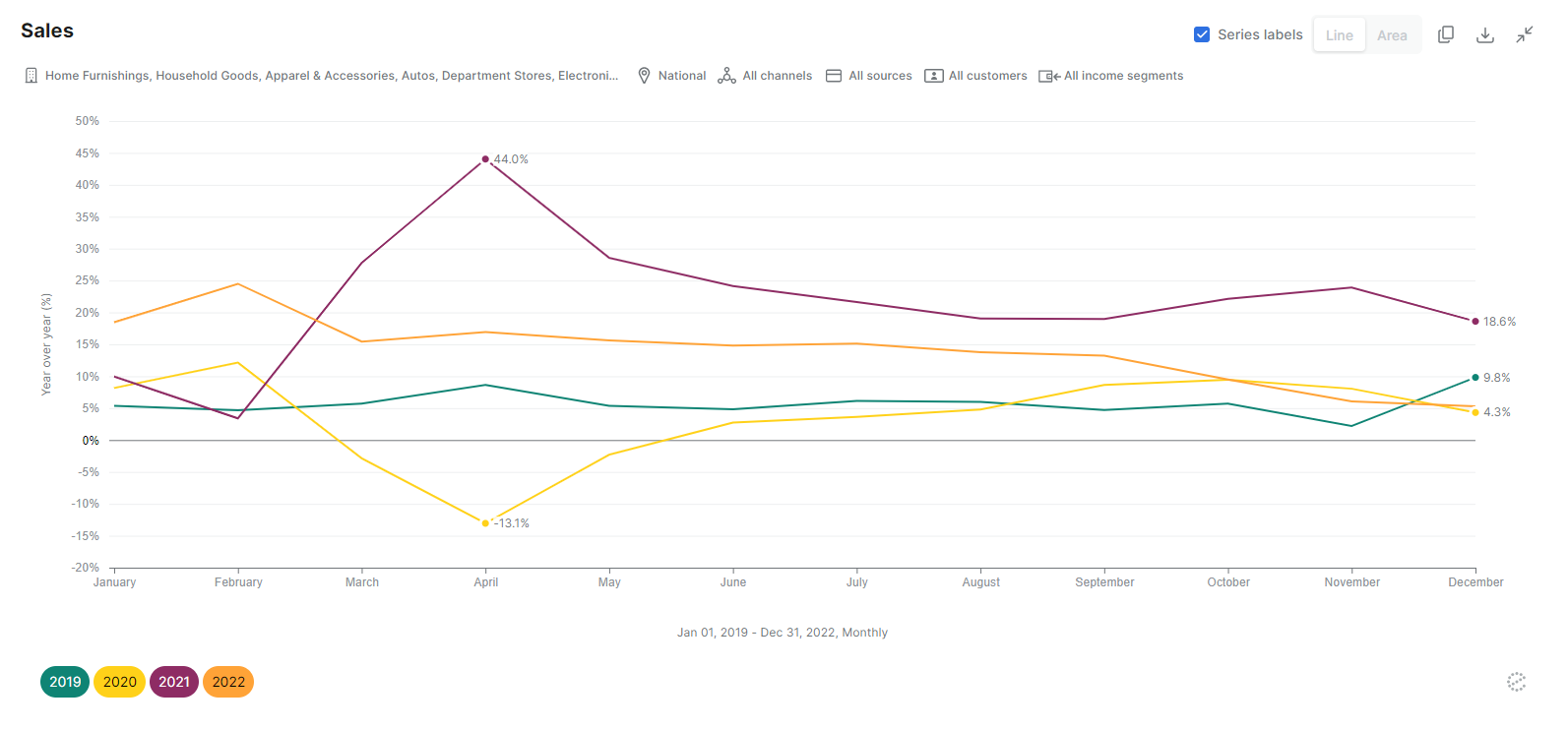

Air Travel, Active & Athleisure, Pet Supplies, Online Marketplaces, and Garden & Outdoor Increase Double Digits

Powered by Earnest’s Vela spend dataset.

Consumers spending increased the fastest on Air Travel, which grew 24% YoY during the 2022 holiday season. Active & Athleisure, Pet Supplies, and Garden & Outdoor continued to outperform and grew double-digits. Online Marketplace spend accelerated 8 points from the preliminary period and was the fourth best performing category for the holiday shopping season. Sports Gear, Footwear, Luxury Apparel, and General Electronics all also accelerated relative to early holiday spend with General Electronics experiencing the largest improvement. Home Fitness, which includes Peloton, stood out as a significant underperformer.

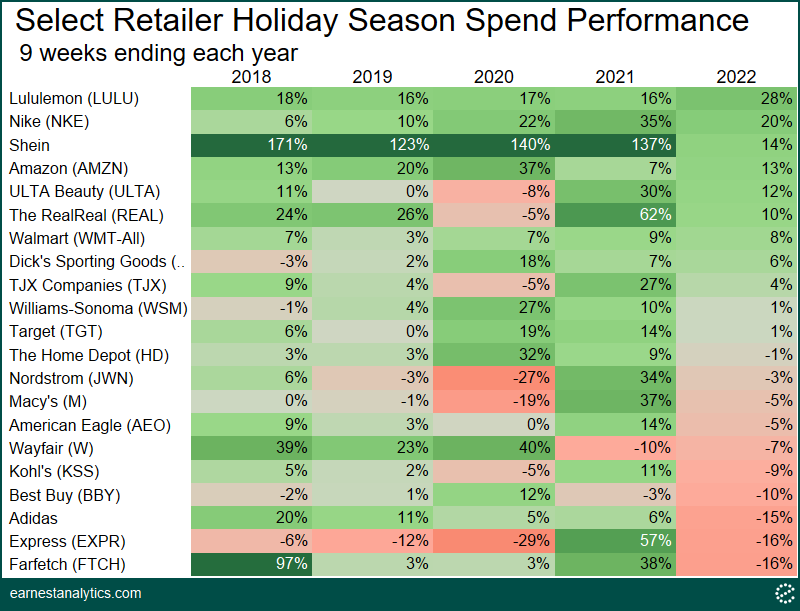

Lululemon, Nike, Shein, The RealReal, and Ulta Beauty Won Share & Led Their Respective Categories

Powered by Earnest’s Vela spend dataset. Analysis done at the parent merchant level.

Consumer spending at Lululemon, Nike, Shein, Amazon, The RealReal, and Ulta Beauty all grew double-digits YoY in the 2022 holiday shopping period. Lululemon and Nike were the fastest growing Active & Athleisure brands posting double-digit gains for the fourth consecutive holiday season. Shein continued to outperform the larger Apparel category, though at a much more normalized YoY pace following several years of tremendous share gains from fast fashion rivals. Amazon returned to mid-teens growth after 2021’s tough comparison to strong pandemic gains. Walmart outgrew Target by 8 points, the first holiday outperformance since 2019 which, given the mix differences between the two (i.e. consumables account for over ~55% of Walmart sales but only ~45% of Target sales), may be the latest sign of non-discretionary outperformance in an inflationary environment.

Express, Farfetch, and Adidas declined mid-teens and performed notably worse than their respective categories, suggesting each lost market share.

Notes

Holiday dates in this analysis defined as 11/1/22-1/2/23 for the 2022 season, 11/2/21-1/3/22 for the 2021 season, 11/3/20-1/4/21 for the 2020 season, 11/5/19-1/6/20 for the 2019 season, 10/30/18-12/31/18 for the 2018 season, and 10/31/17-1/1/18 for the 2017 season. Each period consists of 63 days (9 weeks), beginning on a Tuesday and ending on a Monday. All Merchant performance trends should be interpreted in the context of our EarnestKPI backtest differentials. For a better understanding of the data please schedule a demo.