Holiday Retail 2021 Data Shows Slowing Spend, Earlier Shopping So Far

Key takeaways for holiday retail season 2021

- Consumer spending decelerated, while visits exceeded pre-pandemic levels so far this holiday retail season

- Pre-Black Friday sales at Walmart, Target, Amazon, and others outperformed Cyber-5 as consumers began shopping earlier this year

- Online sales growth stalled for most retailers, but remained historically high

- Full holiday performance could improve if there remain online orders that have been placed but not yet shipped due to supply chain constraints

Spending decelerated while foot traffic surpassed pre-pandemic levels this holiday retail season

Total aggregate consumer spending grew 3% YoY in the week ending Dec 7th according to the Earnest Analytics (FKA Earnest Research) Spend Index (ERSI*), a measure of sales growth for 2,500+ U.S. consumer discretionary and staples businesses. This was a deceleration from the 9% YoY growth during the first 10 days of the preliminary holiday season (Nov 1 to 10th). Strong average transaction size growth, possibly due to inflation or reduced discounting, was partially offset by fewer transactions (-1% YoY), a deceleration from the 6% YoY transaction growth in October.

Foot traffic visits to stores diverged from lower transaction counts, growing 25% YoY the week after Thanksgiving, while lapping a muted 2020. Notably, visits to physical stores exceeded pre-pandemic levels to date this holiday season, growing roughly 7% Yo2Y from November into early December.

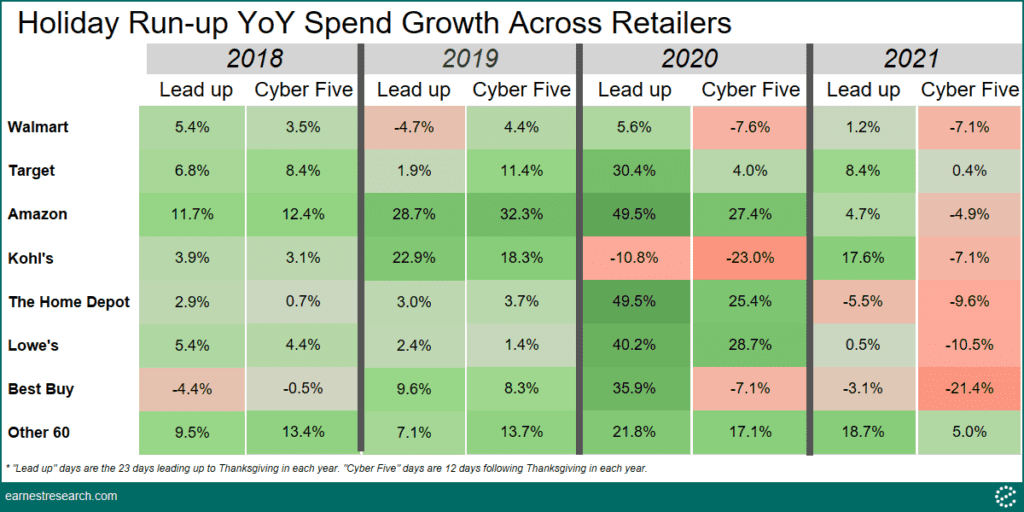

Holiday sales in 2021 happened earlier than years past

Sales growth during the 23-day lead up to Thanksgiving outgrew Cyber-5 sales this year across major retailers, continuing the shift to earlier holiday shopping that began in 2020. Target, Amazon, and Kohl’s sales grew notably during the lead up, while declining YoY in the Cyber-5 period despite consolidating their share of wallet during the five day period.

The Home Depot and Lowe’s sales were flat to down YoY as they lapped the bump from work from home related purchasing surges in 2020 despite data suggesting workers are still staying home. Best Buy sales were slightly down in the lead up to Thanksgiving on tough Covid comps, with Cyber-5 declining significantly more than other major big box stores YoY. Sales growth during the lead up period for 60 other major holiday retailers also outgrew the Cyber-5 period.

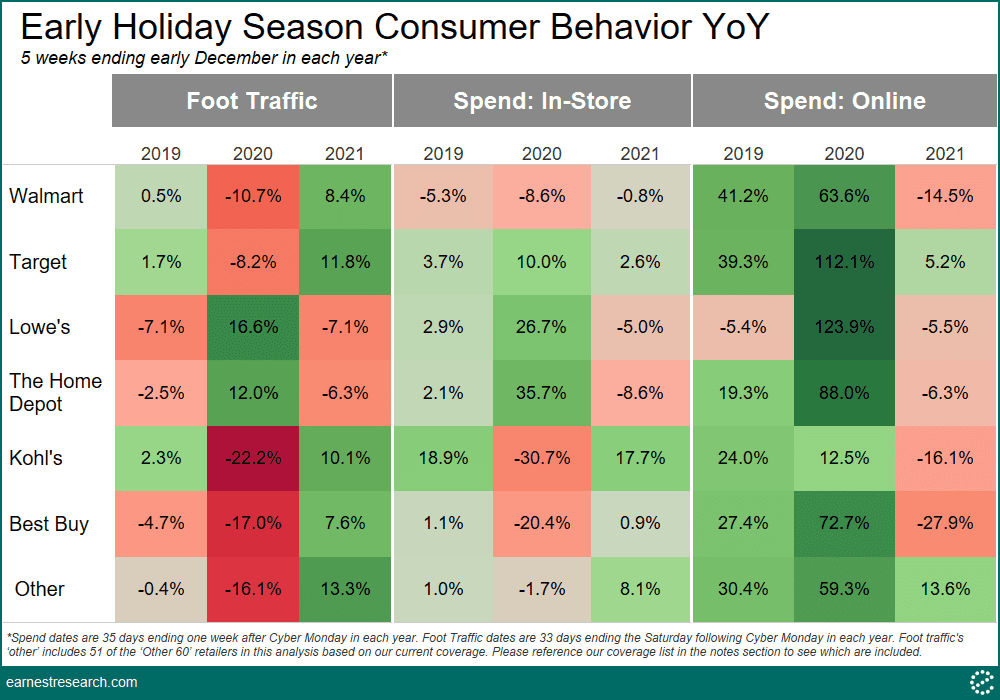

Foot traffic data shows that shoppers returned to brick-and-mortar stores

Foot traffic to Walmart, Target, Kohl’s, and Best Buy grew YoY, marking a clear improvement in in-store spending between 2020 and 2021. Target online sales grew mid single digits, bucking a broader trend of YoY declines compared to 2020 highs. Home brand Lowe’s and The Home Depot bucked the broader trend of recovering in-store visits and spending as they lapped very strong 2020 sales due to work from home related shopping.

Other online spend does not include the travel category, which showed a strong consumer spending on car rentals and lodging in advance of the holiday season.

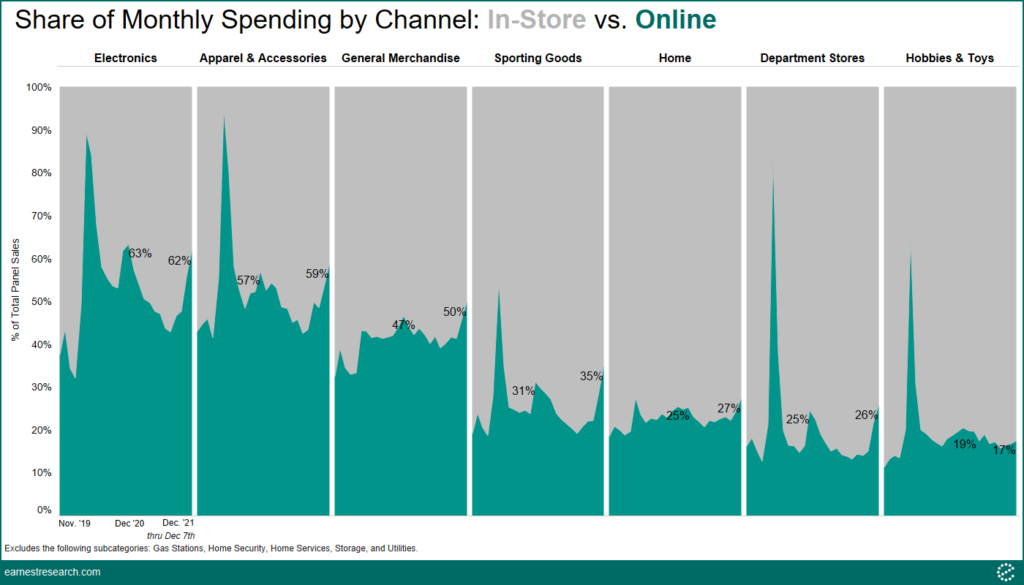

The holidays are the biggest online shopping period of the year… and growing

A higher percentage of total sales occured online during the holiday period than during the rest of year for most categories. That difference between holiday and rest-of-year online sales penetration is particularly pronounced for General Merchandise, Apparel & Accessories, Electronics, Sporting Goods, and Departments Stores, while more consistent for Home and Hobbies & Toys. Among those holiday shopping categories, Apparel & Accessories, Electronics, and General Merchandise stood out, with 50% or more of sales occurring online this holiday season, on par with and even slightly surpassing 2020’s online penetration. Online sales share for all major categories was higher than pre-pandemic.

Online spend data reflects orders that have shipped. Online share of sales and overall growth could improve if orders placed but not yet delivered during the period due to supply chain constraints are fulfilled later in the holiday shopping period.

Notes

- A prior version of this piece contained an error where Walmart’s 2021 performance, particularly its Online channel, was mistakenly inflated. The error has since been corrected.

- *This analysis and our preliminary holiday post employ the proprietary Earnest Analytics (FKA Earnest Research) Spend Index (ERSI) methodology, a measure of consumer spending across 2,500+ large national brands in major consumer discretionary and staples subcategories. Earnest’s broader and proprietary Aggregate Consumer Spending methodology, employed in some of our other research pieces, tracks spending across all captured large, medium, and small size retailers around the country. Holiday trends are similar in both methodologies.

- Analysis excludes spending through captive and cobranded store cards that will likely be paid down after the holiday period. Department Stores included in this analysis are more impacted by this exclusion.

- Walmart throughout this piece includes Walmart Online Grocery.

- All merchant performance trends should be interpreted in the context of our EarnestKPI backtest differentials. For a better understanding of our biases and differentials, please schedule a demo.

- The shortened 2019 holiday season (i.e. there were six fewer days between Thanksgiving and Christmas in 2019 relative to years prior) produced an early ~7 point acceleration due to compressed spending behavior, a dynamic that eventually normalized down as the season progressed. As such, it’s possible this season’s performance will improve, if comparing performance relative to 2019, as the season progresses through.

- Other 60 Retailers include: Academy Sports & Outdoors, Adidas, American Eagle, Ann Taylor, Anthropologie, Audible, Banana Republic, Barnes & Noble, Bath & Body Works, Bed Bath & Beyond, Big Lots, Bloomingdale’s, Burlington Stores, Chewy, Coach, Costco Ex Gas, Crate & Barrel, Dick’s Sporting Goods, Dillard’s, DSW, Etsy, Forever 21, Gap, GNC, H&M, Hobby Lobby, HomeGoods, J.C. Penney, J.Crew, L.L. Bean, Loft, Lululemon, Macy’s, Marshalls, Men’s Wearhouse, Michael Kors, Michaels Stores, Neiman Marcus, Nike, Nordstrom Full Price, Nordstrom Off Price, Old Navy, Overstock.com, Petco ,PetSmart, Pottery Barn, QVC, REI Coop ,Ross Stores, Sam’s Club, Sears, Sephora, Shein, Shopify Payments, Stitch Fix, Stripe, T.J.Maxx, ULTA Beauty, Victoria’s Secret, Wayfair, Williams-Sonoma.